Pix is the instant payments scheme developed, managed and operated by the Central Bank of Brazil....

As the U.S. prepares for continued growth in instant payment transactions with the launch of FedNow in July 2023, it’s valuable to see how instant payments are evolving in other countries that are ahead of the U.S.

Consider Brazil, for example. There are nearly 3 billion Pix instant payment transactions per month in Brazil compared to 17 million RTP instant payments in the U.S. Pix is used by consumers, businesses, and the government to send and receive instant payments.

The Central Bank of Brazil continues to add new features to Pix, the instant payment scheme they mandated and launched in November 2020. The initiatives for the next 24 months include:

- adding a non-priority channel to handle instant payment traffic that doesn’t need to settle immediately

- enhancing the fraud incidences tracked

- adding recurring payments

- requiring new fraud monitoring and restitution measures

These features are designed to make Pix relevant to additional use cases and to enhance the integrity of the overall ecosystem.

Settlement on a non-priority channel

The Central Bank of Brazil is launching a “non-priority channel” for Pix transactions that don’t need to settle instantly. For example, bill payments that are due later in the month will be sent across this non-priority channel and settled later in the day. In-person and e-commerce transactions that must be paid immediately will be sent across the priority channel and settled immediately.

Pix is more efficient and cost effective than other payment methods. This feature will help Pix replace other payment options, especially for enterprise payments that are performed in batches.

This was a change that’s been on their roadmap since the launch of Pix. They aren’t adding this because traffic has slowed or due to any problem. It’s more in anticipation of future growth.

Implications for the U.S.

It’s unlikely that instant payment volume in the U.S. will be high enough to necessitate a non-priority channel in the near term, but it’s something that both The Clearing House and the Federal Reserve may want to consider for the future.

Adding non-Pix fraud incidences to Central Bank’s Directory

The Central Bank of Brazil is expanding the scope of the fraud information they track.

The Directory managed by the Central Bank of Brazil stores over 500 million aliases of consumers and businesses and includes these fields of information.

- Bank Account#

- Branch # (same as routing number in U.S.)

- CPN/CNPJ (similar to SSN/EIN in U.S.)

- Merchant/consumer name

- Name of the financial institution that registered the alias,

- Alias

- Number of fraud transactions associated with that alias.

Pix transactions found to be fraudulent are reported to the Central Bank and are added to their Directory as an incident for the associated alias.

When a Pix Participant starts a Pix transaction, they query the Central Bank’s database and are returned all the information associated with that alias (see above list). If there are too many fraud incidences associated with a certain alias, the Pix Participant can decide not to process the Pix transaction.

If a Pix Participant makes too many queries without executing a Pix transaction, the Central Bank will block them from additional queries because they are likely fishing for personally identifiable information.

In response to this issue, the Central Bank set up a secondary API for querying the database when a Participant only wants to know the number of fraudulent incidences associated with a specific alias. Participants can query this as much as they want without executing Pix transactions and without fear of getting blocked.

With this new Pix release, participants can report fraudulent transactions related to non-Pix activity (e.g. credit card and other account types). When fraud is found, the Financial Institution provides the CPN/CNPJ, the alias as well as the type of fraud to the Central Bank to be added to their Directory.

These non-Pix fraudulent incidences are added together with the Pix fraudulent incidences for specific aliases.

Financial institutions can query the Central Bank’s Directory of Aliases to check the number of fraudulent incidences associated with any alias for non-Pix transactions and account openings.

Implications for the U.S.

As the industry considers a centralized Directory or a “Federated” directory, including stats on fraud incidents may help mitigate fraud overall in instant payments and other financial products.

Recurring Payments (“Pix Automatic”)

This is functionality that will allow users to make recurring payments with Pix. For example, instead of the user paying the monthly Netflix or gym fee using a debit or credit card, the user authorizes the company to automatically request a Pix each month from the paying user's bank, which will automatically trigger a credit transfer from the user's account to the recipient.

This feature will likely go live in 2024. The Central Bank is currently soliciting feedback from Participants on how best to execute this.

As of March 2023, there are three ways being considered for a user to initiate a recurring Pix payment. Examples:

- Amy goes to the gym and asks them to set up recurring payments. The gym’s bank sends this request to Amy’s bank. Amy’s bank messages her asking for approval to automatically trigger a credit transfer from her account to the gym’s account every month.

- Amy gets a bill from her gym with a QR code on the bottom. She scans the QR code and is presented with an option to pay the current bill, or to set up recurring payments.

- The Gym sends Amy a code (somehow) as part of a request for authorization to set up recurring payments. Amy puts this code in her mobile banking app. This triggers a message to be sent to the Gym’s bank to set up recurring payments

Implications for the U.S.

Recurring payments are key to U.S. billers collecting periodic payments from consumers. The Federal Reserve and The Clearing House are rolling out Request for Payments capability that can be structured to enable recurring payments to be processed over FedNow or RTP. As each works with industry participants to configure the process and user experience for RFPs, it’s insightful to learn that Brazil is considering not just one, but three ways the consumer can set up recurring payments.

Also interesting to note that in Brazil there is another option to pay recurring bills called "Débito Automático" (Automatic Debit). However, these recurring transactions can only be processed closed loop where the consumer and the biller have an account at the same financial institution. Because of this, the biggest billers are forced to have accounts at the biggest banks to offer recurring payments. Digital and smaller banks are unable to offer recurring payments to big billers.

This new Pix recurring payments feature will create a standard product for automatic and recurring payments to be processed over the Pix rail. The biller may have an account at Itau, and the consumer at C6 and the recurring payment can be processed by a different financial institution. Ultimately this new feature will create much more competition.

Special Return Mechanism

This new feature aims to increase the likelihood of returning funds to a consumer who was tricked into sending a Pix to a fraudster. It requires that banks monitor up to 5 accounts for 90 days for money that can be reimbursed to a victim.

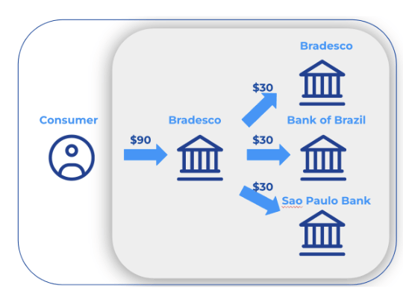

Example:

A consumer with an account at Itau sends a fraudster $90 by Pix to his fraudulent Account A at Bradesco. The fraudster then sends $30 from Account A to Account B at Bradesco, $30 to Account C at Bank of Brazil and $30 to Account D at Sao Paulo Bank. The initial $90 sent to Account A was determined to be a fraudulent transaction. All 4 of these accounts are monitored for 90 days for money that can be returned to the consumer. If Account A gets $90, then $90 is returned to the consumer. If Account B, C or D gets $30, then those funds are returned to the consumer.

Implications for the U.S.

Many in the U.S. believe faster payments will lead to more fraud. Any mechanism to improve the likelihood that an instant payments fraud victim will get their money back would certainly be lauded by U.S. regulators and consumer protection agencies. With that said, many are skeptical that this new initiative will outwit fraudsters as they are quick to move money out of the banking system entirely once they defraud victims. Time will tell how effective this is and whether the U.S. would want to consider a similar program.

Conclusion

Perhaps the most important takeaway from the Pix Roadmap is the continual evolution of Pix functionality. In 2022, there were 24 billion Pix transactions, more than debit card, billet, TED, DOC and check operations combined. Despite the phenomenal growth of Pix, the Central Bank continues to make improvements to what is arguably the most successful instant payments scheme in the world.